Semiconductor in Healthcare Market: Powering the Next Generation of Medical Innovation

1. Market Estimation & Definition

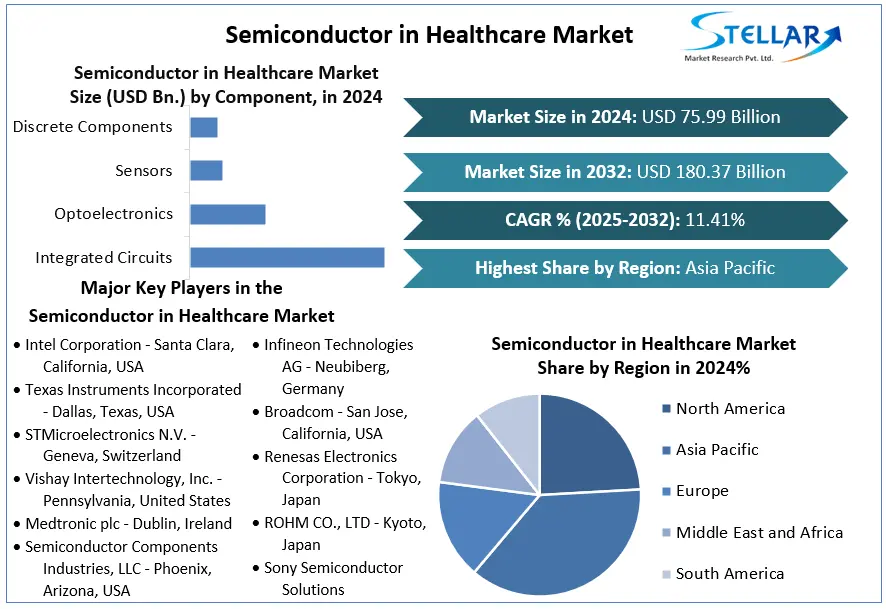

The global Semiconductor in Healthcare Market was valued at approximately USD 75.99 billion in 2024, and is projected to reach nearly USD 180.37 billion by 2032, registering a compound annual growth rate (CAGR) of about 11.41% between 2025 and 2032.

In this context, “semiconductors in healthcare” refers to the use of semiconductor materials and components—such as sensors, integrated circuits (ICs), optoelectronics, discrete devices, MEMS (micro‑electro‑mechanical systems) and mixed‑signal chips—in medical devices, diagnostic instrumentation, patient monitoring systems, therapeutic equipment and health‑IT infrastructure.

These semiconductor components have become foundational to modern healthcare innovations: imaging machines, wearable monitors, remote‑care sensors, lab‑on‑chip diagnostics and connected healthcare systems all rely on advanced semiconductor technology.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/semiconductor-in-healthcare-market/2290

2. Market Growth Drivers & Opportunities

Several strong drivers are underpinning this market’s growth and presenting opportunities:

-

Rise in chronic diseases & aging populations: Healthcare systems globally are under increasing pressure from aging demographics and long‑term conditions (e.g., cardiovascular, diabetes). These drive demand for sophisticated medical devices and monitoring systems that embed semiconductors.

-

Digital health, IoT & connected care: The shift toward remote monitoring, telehealth, wearable sensors and home diagnostics is boosting demand for semiconductor‑enabled sensors, microcontrollers and communications ICs in healthcare

-

Technological miniaturisation & low‑power electronics: Advances in chip‑design, packaging, energy‑efficiency and MEMS sensors allow medical devices to be smaller, more portable and affordable—opening new markets (home, point‑of‑care).

-

Improved imaging & diagnostics: Medical imaging equipment (MRI, CT, ultrasound) require sophisticated semiconductors (optoelectronic detectors, ASICs) for higher resolution and faster scan times—fueling the semiconductor healthcare market.

-

Emerging markets & healthcare infrastructure expansion: Regions such as Asia‑Pacific are investing in healthcare facilities and equipment uptake, creating new demand for semiconductor‑based medical technologies

These drivers highlight both volume growth (more devices, more sensors) and value growth (higher complexity, higher cost chips) for semiconductor suppliers in healthcare.

3. What Lies Ahead: Emerging Trends Shaping the Future

The future of the semiconductor in healthcare market is shaping up around several key trends:

-

Edge‑computing and AI integration in medical devices: Chips that can handle AI, machine‑learning and real‑time analytics at the edge will become more common in diagnostic and monitoring equipment.

-

Wearable & implantable devices: As semiconductors become smaller and more power‑efficient, we will see more advanced wearables and implantables for continuous health monitoring, enabling broader consumer and home‑care use.

-

Lab‑on‑chip and microfluidics: High‑end semiconductor sensors and micro‑electronics will support point‑of‑care diagnostics and personalised medicine.

-

Connected healthcare ecosystems: Semiconductor components will underpin IoT‑based medical devices, remote monitoring networks and smart hospital infrastructure.

-

Advanced imaging and therapy technologies: Semiconductor innovations (e.g., photon counting detectors, enhanced sensor arrays) will push medical imaging into higher precision, lower dose and faster workflows.

-

Regional capacity expansion and localisation: Particularly in Asia‑Pacific, growth will be supported by local manufacturing, government investment in healthcare infrastructure and semiconductor supply‑chain development

For semiconductor companies, this means emphasising healthcare‑certified components, long lifecycle support, and collaboration with medical‑device OEMs.

4. Segmentation Analysis

According to the referenced data:

By Component:

-

Integrated Circuits (ICs)

-

Optoelectronics

-

Sensors

-

Discrete Components

Here, the sensors segment dominated in 2024, reflecting the critical role of sensing in diagnostics, monitoring and smart medical devices.

By Application: -

Medical Imaging

-

Consumer Medical Electronics

-

Diagnostic Patient Monitoring & Therapy

-

Medical Instruments

-

Others

By Region: -

North America

-

Europe

-

Asia‑Pacific

-

Middle East & Africa

-

South America

This segmentation framework shows how stakeholders—from chip manufacturers to device OEMs—can map their strategies by component focus, application end‑use and regional markets.

5. Country‑Level Analysis (Selected)

-

United States (North America): North America is the largest regional market, supported by advanced healthcare infrastructure, high adoption of digital health technologies and strong R&D investment. For example, sensors, wearables and imaging equipment that embed semiconductors are common in U.S. hospitals and home‑care settings.

-

Germany / Europe: Europe ranks high in adoption of premium medical equipment and regulatory standards for healthcare devices. German and other European suppliers of semiconductors in healthcare benefit from strong medical‑device OEM ecosystem and emphasis on device innovation.

-

China / Asia‑Pacific: Asia‑Pacific is projected to grow at the fastest pace, driven by emerging healthcare infrastructure expansion, government programmes for health technology, and localisation of semiconductor manufacturing.

These country‑level insights highlight both mature markets (North America, Europe) and high‑growth markets (Asia‑Pacific) that semiconductor suppliers should prioritise.

6. Commutator (SWOT‑Style) Analysis

Strengths:

-

Semiconductors are critical enablers for modern healthcare technologies—high demand and strong value proposition.

-

Diverse range of applications (imaging, monitoring, diagnostics, wearables) supports broad market addressability.

-

Technological innovation (miniaturisation, connectivity, AI) drives higher complexity and margin expansion.

Weaknesses: -

Medical device regulatory requirements can slow time‑to‑market for semiconductor components designed for healthcare.

-

Medical‑grade semiconductors often require long lifecycle support, high reliability and certification—raising cost and entry barrier.

Opportunities: -

Growth of home‑health, telemedicine and wearable sensors expands addressable market beyond hospitals.

-

Expansion into emerging markets with rising healthcare spend, growing middle class and device uptake (especially in Asia‑Pacific).

-

Strategic partnerships between semiconductor companies and medical‑device OEMs to co‑develop healthcare‑specific chips/sensors.

Threats: -

Supply chain disruptions, component shortages or geopolitical risks could affect availability or cost of semiconductors.

-

Rapid technology change (e.g., alternative materials, new sensor technologies) may require heavy investment and carry risk.

-

Cost pressures in healthcare budgets may delay procurement of next‑generation devices, impacting component demand.

7. Press Release Conclusion

The Semiconductor in Healthcare Market stands at a transformative intersection of medical innovation and micro‑electronics. With a base valuation of about USD 75.99 billion in 2024 and steep growth forecast to nearly USD 180.37 billion by 2032 (CAGR ~11.41%), the market offers significant opportunity for semiconductor firms, medical‑device manufacturers and healthcare stakeholders.

As healthcare delivery shifts toward connected, personalised, portable and data‑driven models, semiconductors become the invisible but indispensable backbone. Device manufacturers and chip suppliers who focus on certified, reliable, healthcare‑optimised semiconductors, embrace partnerships, and align with regional growth markets will capture substantial value.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

sales@stellarmr.com

Warning: Undefined array key "_is_photo" in /home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/9ea4999d05077b6b690d81624544cd64a51b1299_0.file.__feeds_post.comments.tpl.php on line 27

Warning: Attempt to read property "value" on null in /home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/9ea4999d05077b6b690d81624544cd64a51b1299_0.file.__feeds_post.comments.tpl.php on line 27

" style="background-image:url(

Warning: Undefined array key "user_picture" in /home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/19bd7b5d2fc32801d9316dbc2d8c5b25c99e72c3_0.file.__feeds_comment.form.tpl.php on line 31

);">

/home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/9ea4999d05077b6b690d81624544cd64a51b1299_0.file.__feeds_post.comments.tpl.php on line 128

Warning: Attempt to read property "value" on null in /home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/9ea4999d05077b6b690d81624544cd64a51b1299_0.file.__feeds_post.comments.tpl.php on line 128

">