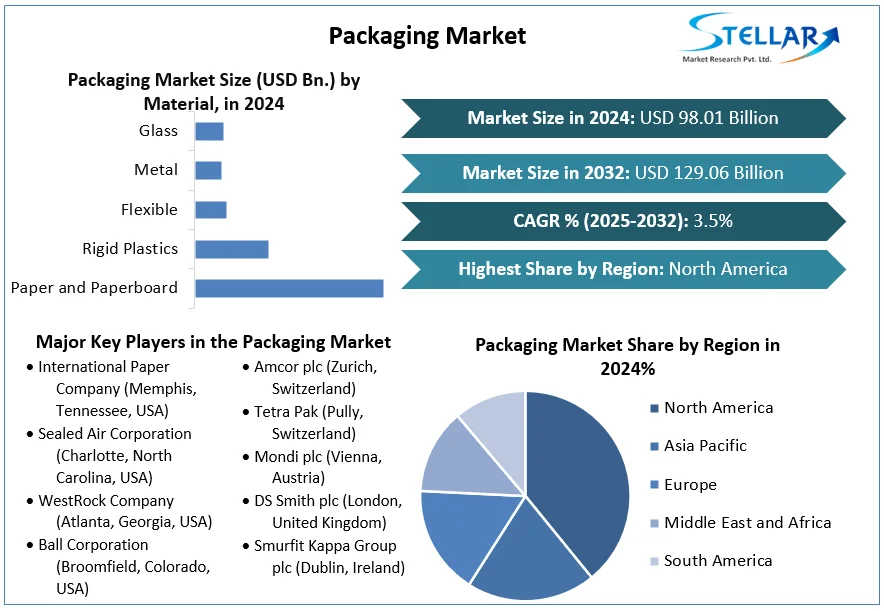

A comprehensive new analysis of the global packaging market reveals a period of steady, large-scale growth underpinned by fundamental global consumption and powerful industry shifts. The market, valued at USD 98.01 Billion in 2024, is expected to grow at a compound annual growth rate (CAGR) of 3.5% from 2025 to 2032, reaching nearly USD 129.06 Billion. This expansion highlights packaging's indispensable role in the global economy, serving critical functions of protection, preservation, and marketing across every consumer and industrial sector. The market's evolution is increasingly defined by the dual forces of booming e-commerce and a decisive global pivot toward sustainable and circular packaging solutions.

Purchase This Research Report at up to 30% Off @ https://www.stellarmr.com/report/req_sample/Packaging-Market/1869

Market Estimation & Definition

The global packaging market encompasses the vast ecosystem of materials, designs, and systems used to contain, protect, preserve, transport, inform, and merchandise products. It is defined by its essential function in enabling global trade, ensuring product safety, and communicating brand value. With a colossal valuation of USD 98.01 Billion in 2024, the market is a foundational pillar of modern commerce. The projected growth to over USD 129 Billion by 2032 reflects sustained demand driven by global megatrends including urbanization, population growth, rising consumption, and the digital transformation of retail. This growth is increasingly shaped by consumer and regulatory demands for packaging that performs its traditional roles while minimizing environmental impact.

Market Growth Drivers & Opportunity

The market is propelled by two transformative and interconnected megatrends. The explosive, sustained growth of e-commerce is fundamentally reshaping packaging demand, particularly for durable, protective, and efficient transit solutions like corrugated boxes. This channel demands packaging that can survive the supply chain while also addressing consumer concerns about excessive material use. Concurrently, intensifying global focus on sustainability is the single most powerful driver of innovation and investment. Consumers, brands, and regulators are demanding a reduction in packaging waste, a shift to recyclable and compostable materials, and the development of a true circular economy for packaging.

A monumental market opportunity lies in the development and adoption of next-generation sustainable materials. The surge in bioplastics and novel polymers like PEF (polyethylene furanoate)—which is 100% bio-based and offers superior barrier properties—represents a frontier for replacing conventional plastics. Furthermore, the strategic transition from rigid to optimized flexible packaging formats offers significant opportunities to reduce material usage and carbon footprint while maintaining product integrity, a key focus for leading converters and brands. The implementation of ambitious regulatory frameworks, such as the European Union's Circular Economy Action Plan, is creating a structured push for innovation across the entire packaging value chain.

What Lies Ahead: Emerging Trends Shaping the Future

The future of the packaging market will be characterized by material science breakthroughs, smart system design, and the relentless pursuit of circularity. Material innovation will accelerate, with advanced bioplastics, fiber-based solutions, and lightweight composites competing to meet performance and sustainability benchmarks. The industry will see a stronger systemic focus on designing for recyclability and reuse, moving beyond single-life cycles to models that incorporate refillable systems, standardized containers, and efficient recovery infrastructure, especially in metal and glass packaging.

Furthermore, e-commerce will continue to be a primary engine of design evolution, driving needs for right-sized packaging, innovative protective functions (cushioning, blocking, bracing), and consumer-unboxing experiences that balance protection with minimal waste. However, the industry faces the complex, ongoing challenge of navigating a global patchwork of regulations on plastics, extended producer responsibility (EPR), and recycling targets, which requires agility and proactive strategy from multinational players.

Segmentation Analysis

The market is segmented by Material, Function, and Application, revealing the core building blocks of the industry.

-

By Material: Paper and Paperboard commanded the highest market share in 2024 and are poised to continue their dominance. This leadership is driven by the material's renewable nature, high recyclability, versatility (from corrugated boxes to liquid cartons), and its essential role in e-commerce logistics. Other key materials include Rigid Plastics, Flexible Packaging, Metal, and Glass, each selected for specific product needs like barrier properties, durability, or premium presentation.

-

By Function: Packaging serves multiple technical roles including Cushioning, Blocking & Bracing, Void Fill, Insulation, and Wrapping. The growth of e-commerce and complex global supply chains is increasing demand for high-performance protective functions.

-

By Application: Key end-use sectors are Food, Beverage, Healthcare, Cosmetics, and Industrial. The food and beverage segment represents the largest application area, driven by global consumption, safety requirements, and the need for convenience formats.

Purchase This Research Report at up to 30% Off @ https://www.stellarmr.com/report/req_sample/Packaging-Market/1869

Country-Level Analysis for the USA and Germany

The competitive landscape is composed of global integrated players and regional specialists, with heavy concentration in North America and Europe.

-

In the United States, the core of the leading North American market, major players include International Paper Company, WestRock Company, Berry Global Group, Inc., and Ball Corporation. The U.S. market is characterized by a strong focus on sustainability initiatives, a mature recycling infrastructure (though evolving), massive e-commerce volume, and significant investment in R&D for innovative and lightweight packaging solutions.

-

In Germany, a powerhouse within the sophisticated European market, key players include global leaders like Amcor plc and specialized firms such as Huhtamäki Oyj. The European market is defined by some of the world's most stringent environmental regulations (like the EU Circular Economy Action Plan), high consumer awareness, and advanced collection and recycling systems, which drive innovation in design-for-recycling and reusable models.

Other notable global competitors include Tetra Pak (Switzerland) in liquid cartons, DS Smith plc (UK) in corrugated and recycling, and Mondi plc (Austria) as a global leader in sustainable packaging. In the Asia-Pacific region, giants like Oji Holdings Corporation (Japan) are major forces in paper and packaging.

Competitive Analysis

Competition in the packaging market is fierce and revolves around scale, innovation, and sustainability leadership. Large, integrated players compete on global supply chain efficiency, vast manufacturing scale, and the ability to offer a full portfolio of material solutions to multinational brand customers. A critical competitive battleground is technology and material innovation, with companies racing to develop and commercialize sustainable alternatives—such as high-barrier recyclable films, advanced bioplastics, and lightweighted containers—that meet brand and regulatory demands.

Sustainability credentials have become a primary differentiator. Companies compete through ambitious public commitments (e.g., to net-zero, recycled content, or recyclability goals), investments in recycling infrastructure, and the development of circular business models. Strategic growth is also pursued through targeted mergers and acquisitions to acquire new technologies (like digital printing or smart packaging), enter high-growth geographic markets, or consolidate market position in specific material segments, as seen in recent industry transactions.

Press Release Conclusion

The trajectory of the global packaging market confirms its massive scale and essential role, steadily advancing toward USD 129 Billion by 2032. This growth, however, is occurring within a paradigm shift where environmental performance is now as critical as functionality and cost. The industry's future will be won by those who can successfully navigate the tension between fulfilling its traditional protective and commercial roles while radically reducing its environmental footprint. Success hinges on mastering circular design, championing material science breakthroughs, building resilient and efficient supply chains for both virgin and recycled materials, and forging deep collaborations across the value chain—from material producers and converters to brands, retailers, recyclers, and policymakers. For stakeholders, the path forward is clear: investment in sustainable innovation is no longer optional but the core driver of long-term competitiveness and license to operate in the global market.

ng alternatives to smoking. For stakeholders, the snus market represents a stable but challenging segment where deep regulatory understanding is just as important as product quality.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

sales@stellarmr.com

Warning: Undefined array key "_is_photo" in /home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/9ea4999d05077b6b690d81624544cd64a51b1299_0.file.__feeds_post.comments.tpl.php on line 27

Warning: Attempt to read property "value" on null in /home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/9ea4999d05077b6b690d81624544cd64a51b1299_0.file.__feeds_post.comments.tpl.php on line 27

" style="background-image:url(

Warning: Undefined array key "user_picture" in /home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/19bd7b5d2fc32801d9316dbc2d8c5b25c99e72c3_0.file.__feeds_comment.form.tpl.php on line 31

);">

/home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/9ea4999d05077b6b690d81624544cd64a51b1299_0.file.__feeds_post.comments.tpl.php on line 128

Warning: Attempt to read property "value" on null in /home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/9ea4999d05077b6b690d81624544cd64a51b1299_0.file.__feeds_post.comments.tpl.php on line 128

">