Asia-Pacific Bio-Butanol Market Emerges as a Strategic Frontier for Green Chemicals and Fuels

A new industry report highlights the burgeoning potential of the Bio-Butanol market in the Asia-Pacific region, positioning it as a key component in the transition toward sustainable chemicals and biofuels. The market is projected to grow at a promising compound annual growth rate (CAGR), driven by environmental mandates, technological advances, and the search for non-fossil feedstocks.

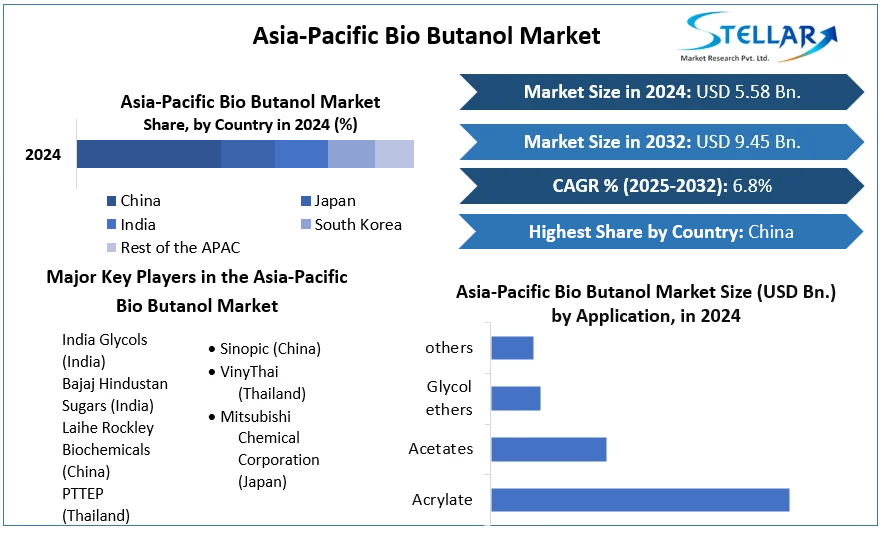

Purchase This Research Report at up to 30% Off @ https://www.stellarmr.com/report/req_sample/Asia-Pacific-Bio-Butanol-Market/1212a

Market Estimation & Definition

The Asia-Pacific Bio-Butanol market encompasses the production and application of butanol (C₄H₉OH) derived from renewable biomass sources, as opposed to traditional petrochemical routes. It is produced through the fermentation of sugars from feedstocks like corn, sugarcane, cassava, or agricultural waste (second-generation) using specialized microbes like Clostridium acetobutylicum (ABE fermentation). The market is defined by its value proposition as a "green" chemical building block and a potential advanced biofuel with superior properties to ethanol. It serves as a renewable alternative for producing solvents, plasticizers, coatings, and as a blendstock for gasoline, offering a path to decarbonize multiple industrial value chains.

Market Growth Drivers & Opportunity

The market's primary catalyst is the intensifying global and regional push for sustainability and carbon reduction. Government policies supporting biofuels and bio-based products, such as blending mandates and low-carbon fuel standards, are creating a regulatory pull for alternatives like bio-butanol. This is coupled with the growing corporate demand for sustainable sourcing and green chemistry from major chemical, paint, and coating manufacturers seeking to reduce their carbon footprint and meet ESG (Environmental, Social, and Governance) goals.

Significant opportunities are anchored in technological breakthroughs and regional feedstock advantages. Advances in fermentation efficiency, novel microbial strains, and the successful commercialization of second-generation (2G) technologies that use non-food biomass (like rice straw, bagasse, wood chips) are critical to improving economics and sustainability credentials. The Asia-Pacific region, with its vast agricultural resources and biomass waste streams, is uniquely positioned to become a low-cost production hub if these technologies mature. Furthermore, bio-butanol's superior fuel properties—higher energy content, lower corrosivity, and better blending capability with gasoline than ethanol—present a compelling opportunity in the transportation fuel sector, particularly for countries aiming to deepen their biofuel penetration.

What Lies Ahead: Emerging Trends Shaping the Future

The future of bio-butanol in Asia-Pacific hinges on cost-competitiveness and integrated biorefinery models. A dominant trend is the drive toward integrated biorefineries and co-production strategies. To improve economics, producers are looking to co-produce bio-butanol alongside other high-value bioproducts like acetone, ethanol (from the ABE process), or bio-succinic acid, maximizing revenue from the same feedstock and process infrastructure. This is closely linked to the strategic focus on non-food, waste-based feedstocks to avoid the "food vs. fuel" debate and tap into low-cost, abundant raw materials like agricultural residues, which is a major focus of R&D in the region.

The competitive and investment landscape is also characterized by strategic partnerships and pilot-scale validation. The path to commercialization requires collaboration between biotechnology startups, established chemical companies, energy majors, and government research institutes. Success depends on scaling pilot plants to demonstration and commercial scale, securing offtake agreements with large industrial users, and navigating complex sustainability certification pathways. The high capital intensity and technical risk mean that government grants, green financing, and patient strategic capital will be essential to bridge the "valley of death" for new projects.

Segmentation Analysis

The market is segmented by feedstock, application, and end-use industry:

-

By Feedstock: The market is divided into First-Generation (Food-Based) feedstocks like corn, sugarcane, and cassava, and Second-Generation (Non-Food) feedstocks like agricultural residues (straw, stover), dedicated energy crops, and municipal solid waste. While 1G dominates current pilot projects due to established supply chains, 2G is the critical long-term growth segment for sustainable scalability.

-

By Application: Key applications include Biofuel/ Fuel Additives (as a gasoline blendstock or standalone fuel), Industrial Solvents (a direct replacement for petroleum-based butanol in paints, coatings, and cleaners), and as a Chemical Intermediate for producing bio-based plastics (e.g., butyl acrylate), plasticizers, and other derivatives.

-

By End-Use Industry: The Transportation Fuels sector represents a high-volume potential market. The Paints & Coatings Industry is a key early-adopter segment for green solvents. The Plastics & Polymers Industry is a target for bio-based intermediates. The Chemical Industry at large is the overarching consumer for butanol as a platform chemical.

Country-Level Analysis

-

China: China is poised to be a central player, driven by its national strategic focus on biomass utilization, energy security, and combating pollution. Strong government support for advanced biofuels within its ethanol blending program and "Dual Carbon" goals could provide a significant demand pull. China also has substantial agricultural and forestry residues, making it a prime location for 2G bio-butanol development if technology matures.

-

India: India presents a massive opportunity due to its government's strong push for biofuels (National Biofuel Policy), its vast sugarcane and rice straw residue volumes, and a large domestic market for chemicals and fuels. The success of first-generation ethanol provides a policy framework and infrastructure that could be leveraged for bio-butanol. R&D initiatives and public-private partnerships are key to advancing the technology locally.

-

Japan: Japan, with limited biomass resources but advanced biotechnology capabilities and a strong corporate drive for sustainability, is likely to be a technology innovator and a consumer of high-value, certified bio-based chemicals. Japanese chemical companies may invest in or partner with production ventures in biomass-rich neighboring countries to secure supply.

-

Thailand & Malaysia: These Southeast Asian nations, with their large palm oil and sugarcane industries, have significant biomass waste streams (empty fruit bunches, bagasse) that could feed 2G bio-butanol plants. Their established agro-industrial sectors provide a foundation for developing integrated biorefineries.

Competitive Analysis

The competitive landscape is in a formative stage, dominated by biotechnology developers, research consortia, and early-mover energy/chemical companies. Pure-play bio-butanol technology firms like Butamax Advanced Biofuels (a JV between BP and DuPont) and Gevo, Inc. are actively seeking global partnerships, including in Asia-Pacific. Regionally, the competition will come from state-owned energy giants (like CNPC, Sinopec in China), large agro-industrial conglomerates (like Mitr Phol in Thailand or Wilmar in Singapore/Malaysia), and specialized biotechnology startups emerging from regional research institutes. Competition at this stage is less about market share and more about technology validation, securing strategic partners, demonstrating production economics at scale, and establishing first-mover advantages in key markets. Success hinges on forming alliances across the value chain—from feedstock suppliers to offtakers—and navigating supportive policy environments.

Press Release Conclusion

The Asia-Pacific Bio-Butanol market represents a high-potential but challenging frontier in the bioeconomy. Its growth is inextricably linked to the region's ability to leverage its biomass resources, master advanced fermentation technology, and create a supportive policy and investment ecosystem. While the technical and economic hurdles to widespread commercialization are significant, the drivers of decarbonization and sustainable industrial production are powerful and enduring. The companies and countries that can successfully integrate innovative biology with industrial scale and forge strong supply chain partnerships will be well-positioned to capture value in this emerging green market. Bio-butanol may not replace its petroleum counterpart overnight, but it is carving out a vital role as a versatile, renewable molecule in the future low-carbon economy of Asia-Pacific.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

sales@stellarmr.com

Warning: Undefined array key "_is_photo" in /home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/9ea4999d05077b6b690d81624544cd64a51b1299_0.file.__feeds_post.comments.tpl.php on line 27

Warning: Attempt to read property "value" on null in /home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/9ea4999d05077b6b690d81624544cd64a51b1299_0.file.__feeds_post.comments.tpl.php on line 27

" style="background-image:url(

Warning: Undefined array key "user_picture" in /home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/19bd7b5d2fc32801d9316dbc2d8c5b25c99e72c3_0.file.__feeds_comment.form.tpl.php on line 31

);">

/home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/9ea4999d05077b6b690d81624544cd64a51b1299_0.file.__feeds_post.comments.tpl.php on line 128

Warning: Attempt to read property "value" on null in /home/senmarri/public_html/friend24.in/content/themes/default/templates_compiled/9ea4999d05077b6b690d81624544cd64a51b1299_0.file.__feeds_post.comments.tpl.php on line 128

">